Why I’m Not Betting on a Soft Landing

Why I’m Not Betting on a Soft Landing

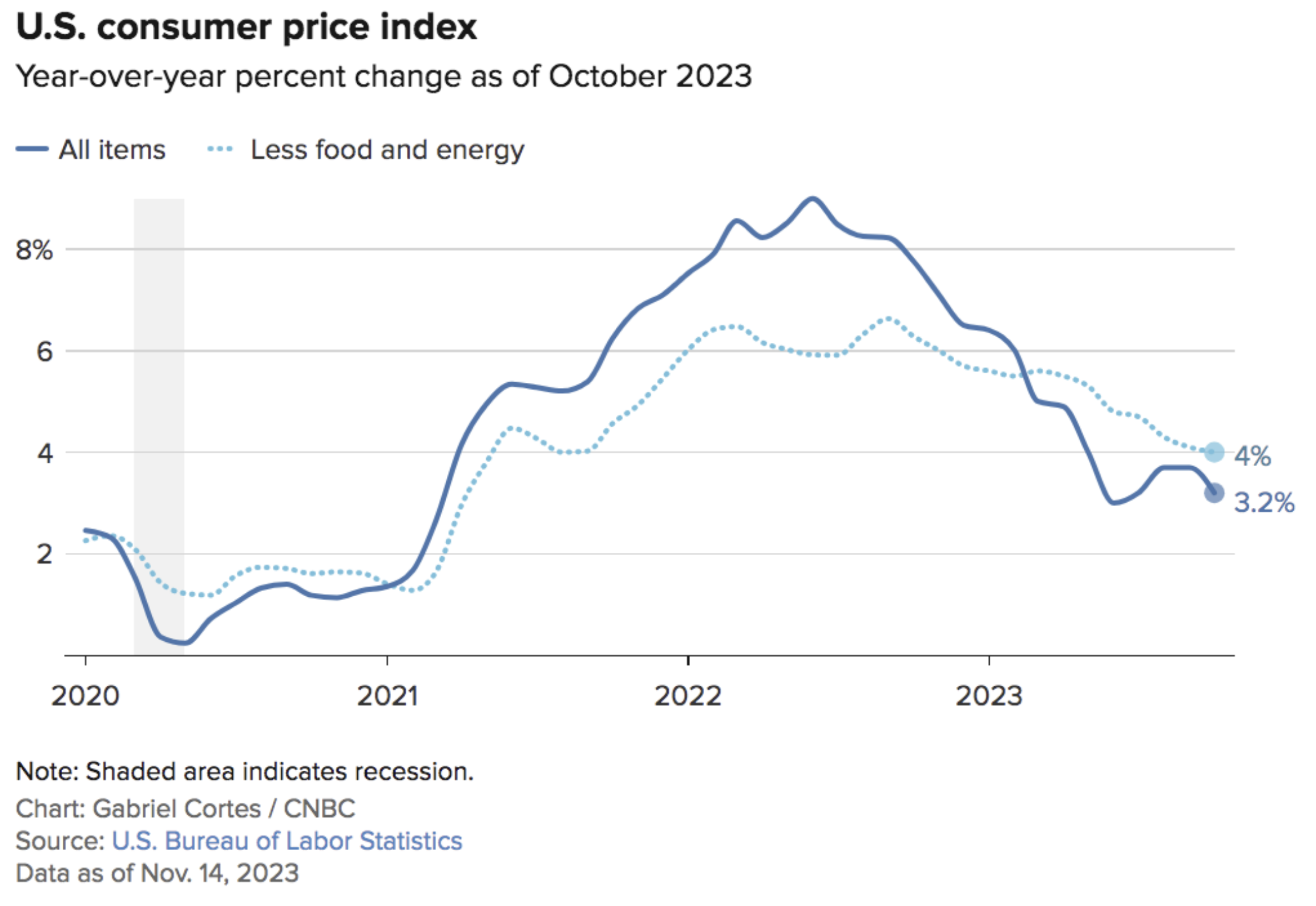

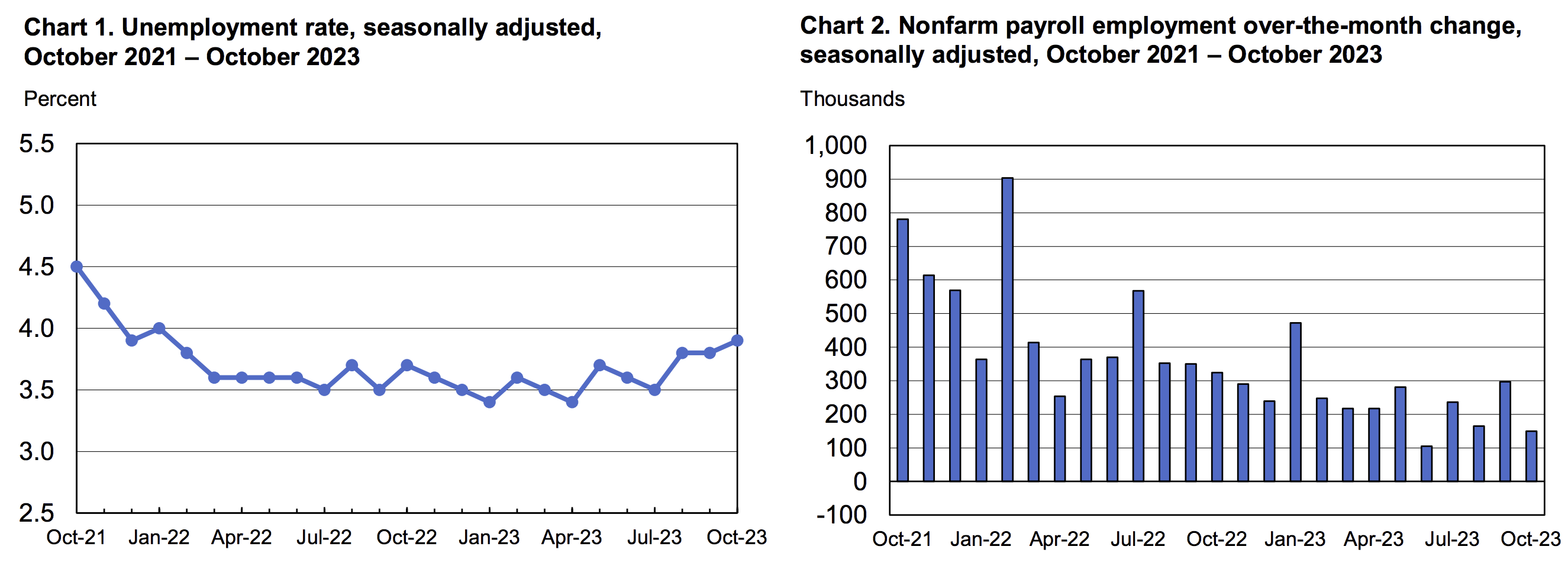

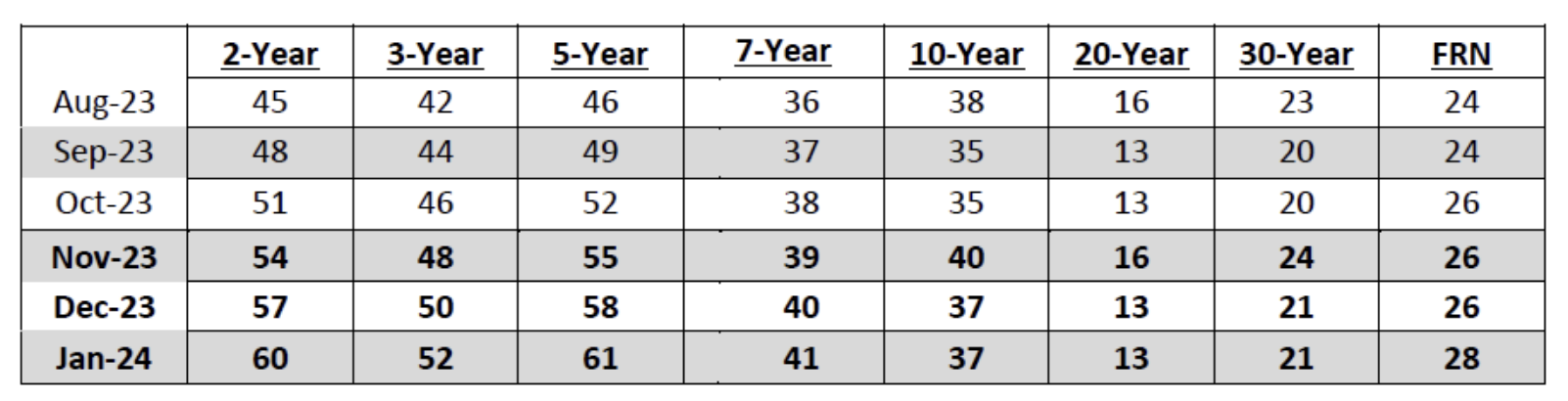

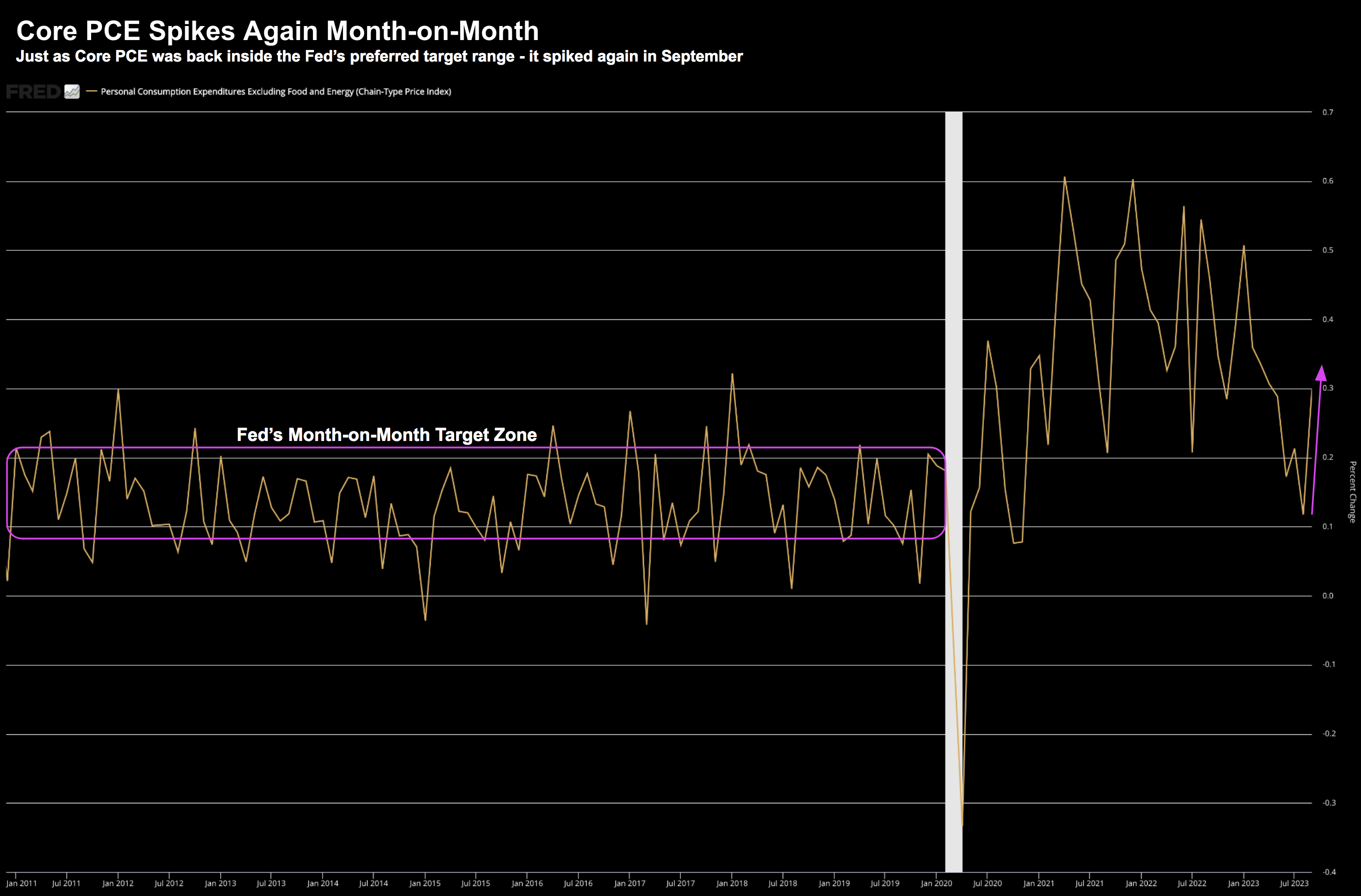

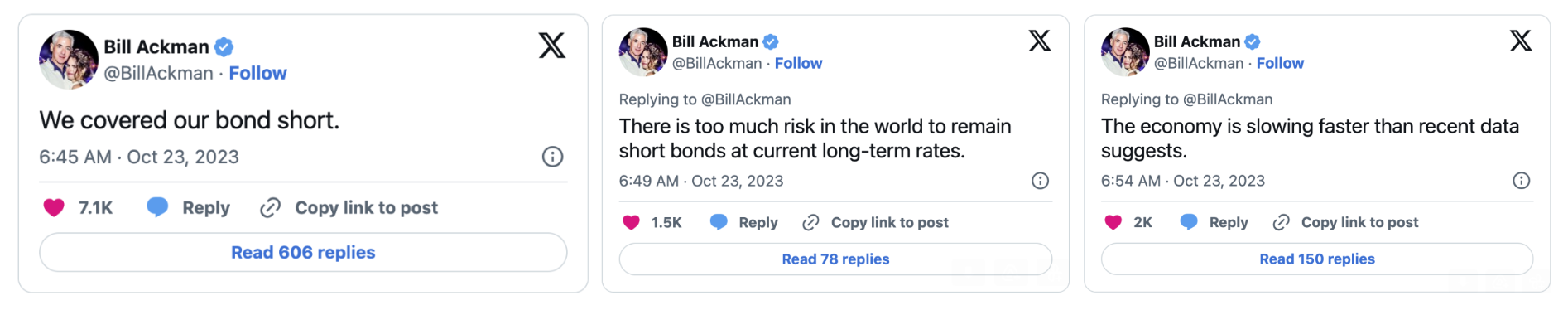

With the Fed seemingly on pause and bond yields sharply off their highs - markets are optimistic. Equities have surged the past few weeks - up around 17.6% year-to-date. The S&P 500 added 10% in just 3 weeks! The narrative (as far as I can tell) is we're headed for "soft landing". But can we be so sure? Past experience suggests a "hard landing" is the more likely outcome. And absent other evidence, when the Fed hikes this much (and especially this fast) - we should expect one.