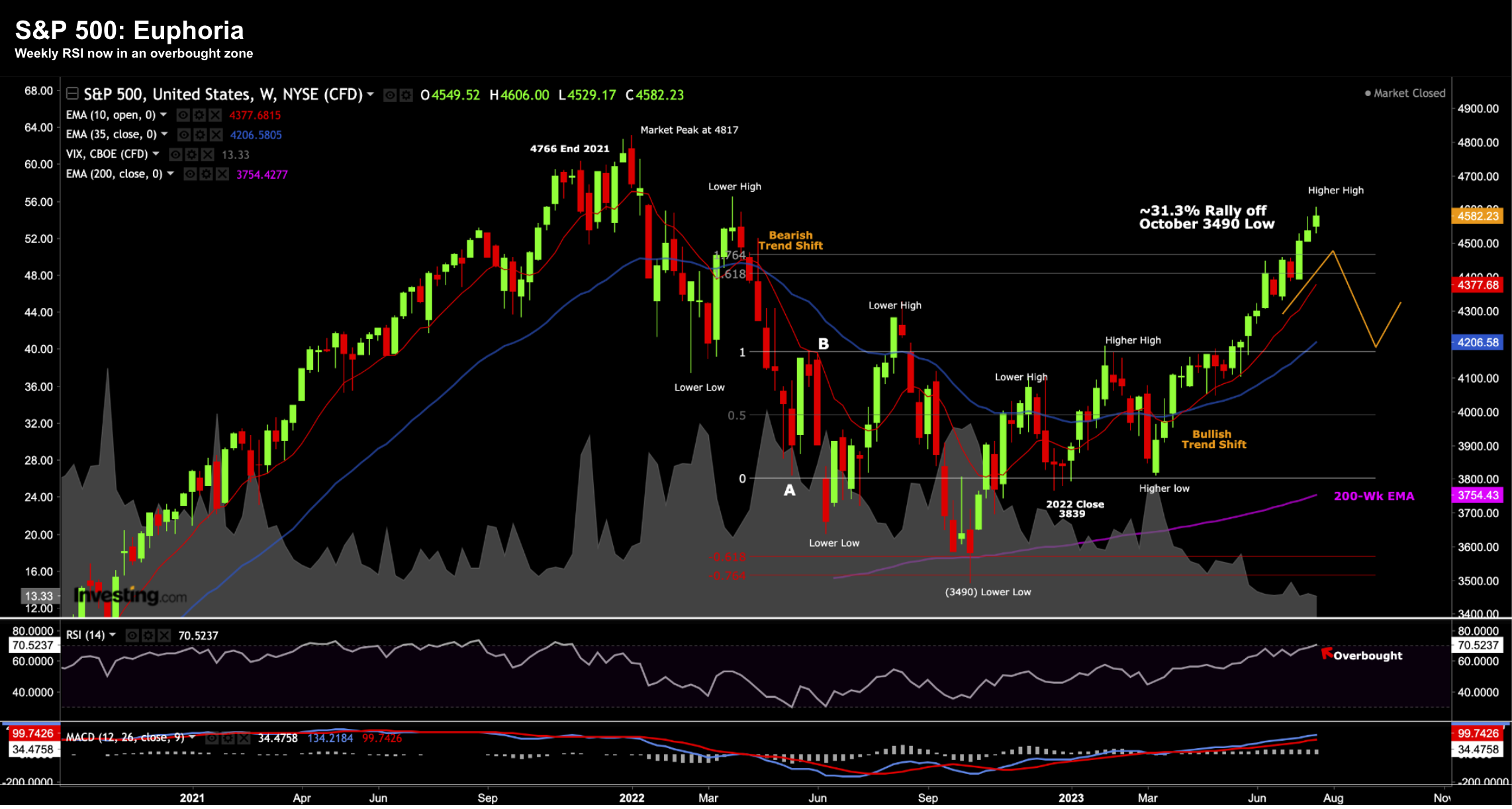

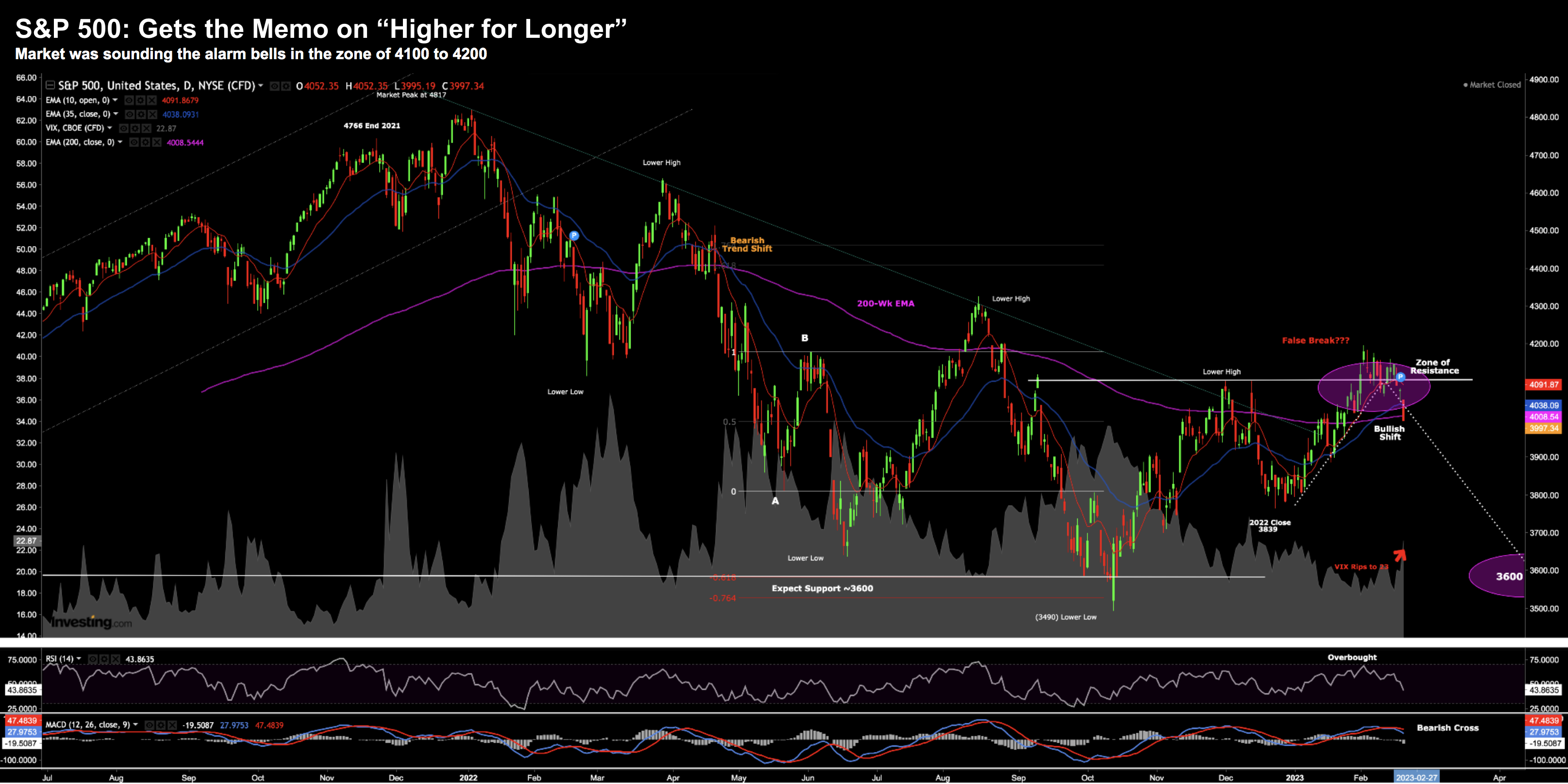

The Battle-lines are Drawn

The Battle-lines are Drawn

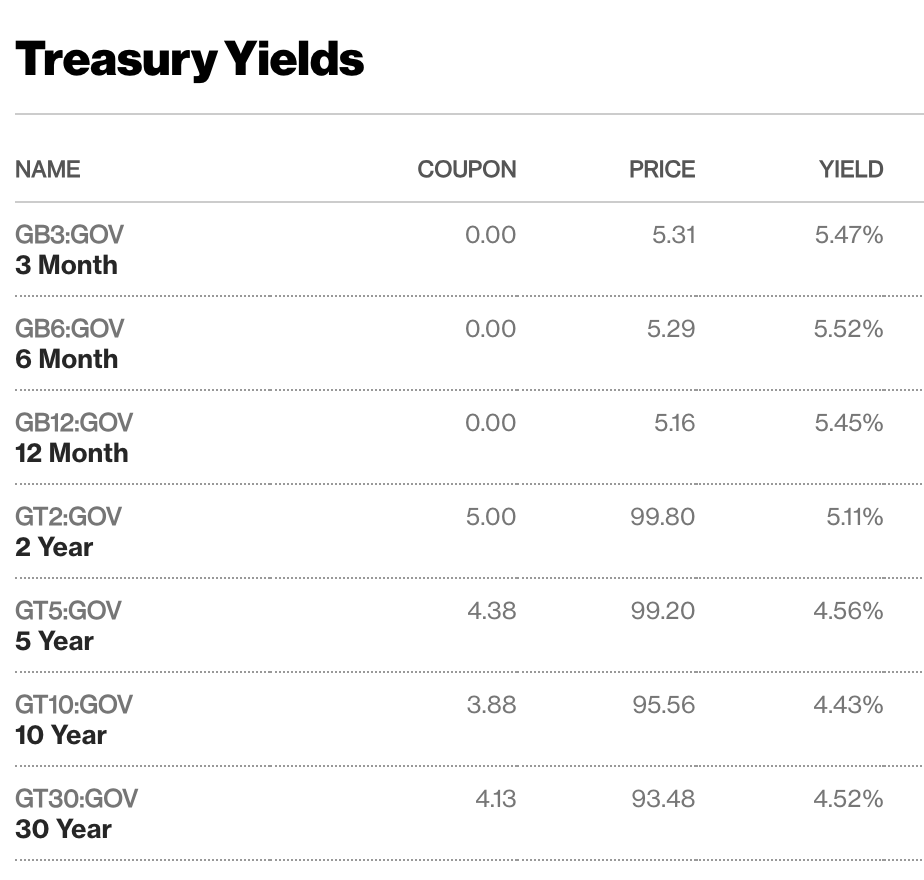

Here's today's question: do you think 18.3x forward earnings is a good risk/reward bet? For me, the answer is no. And I say this because investors have a very compelling alternative. We don't need to look any further than bond yields. For example, the 12-month US treasury yield offers investors 5.45%