Is it Still Going to be a “Soft Landing”?

Is it Still Going to be a “Soft Landing”?

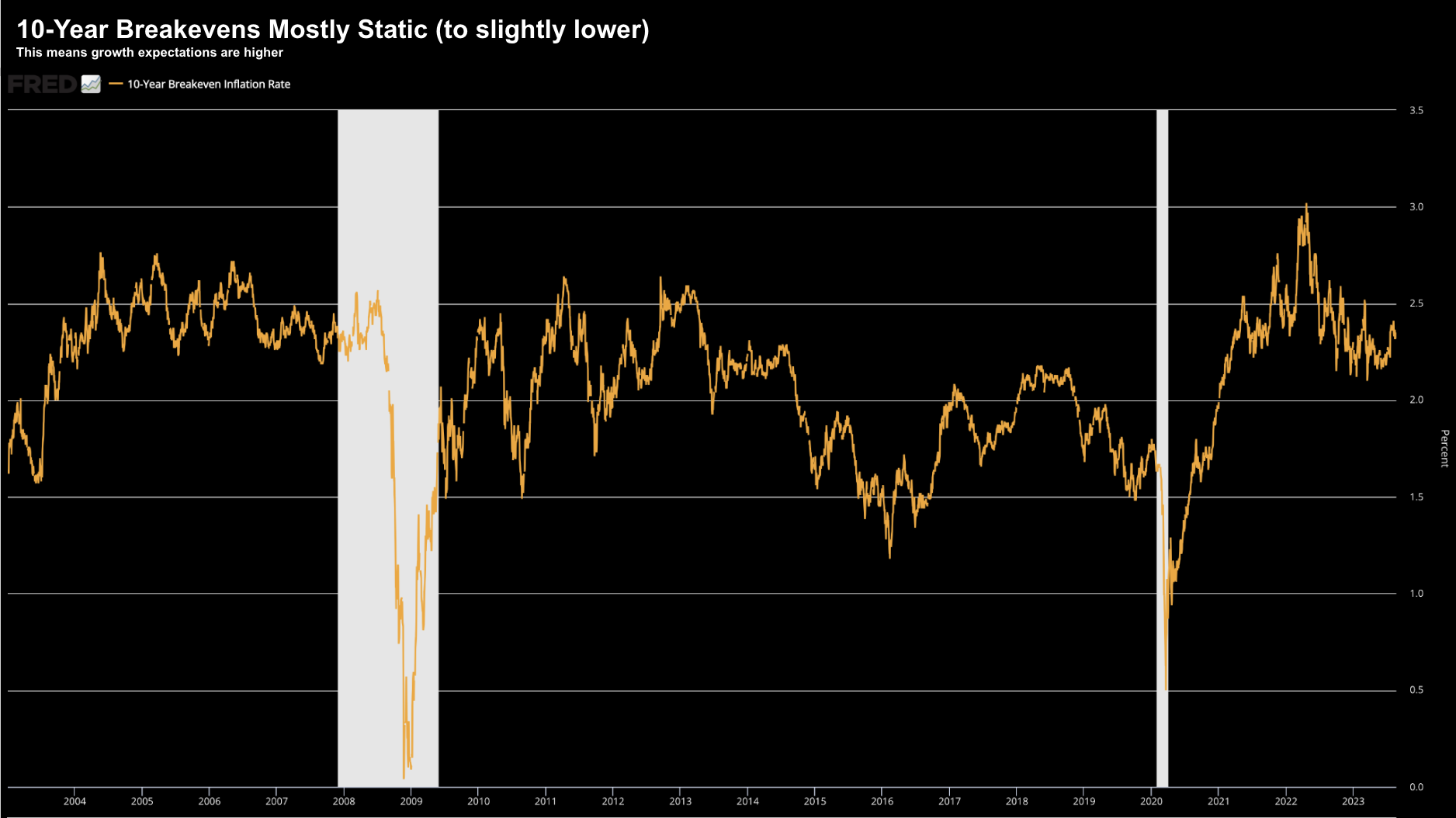

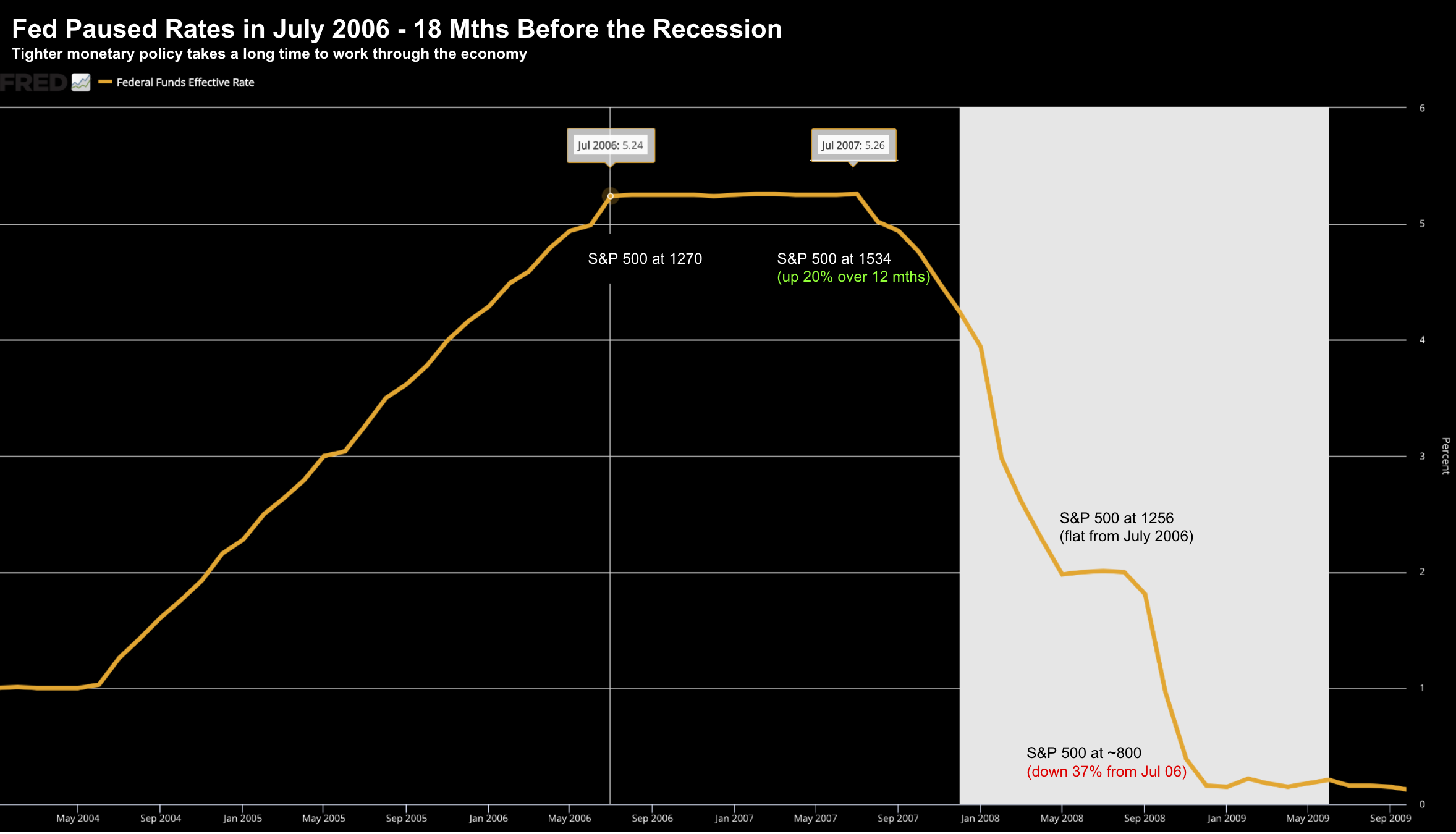

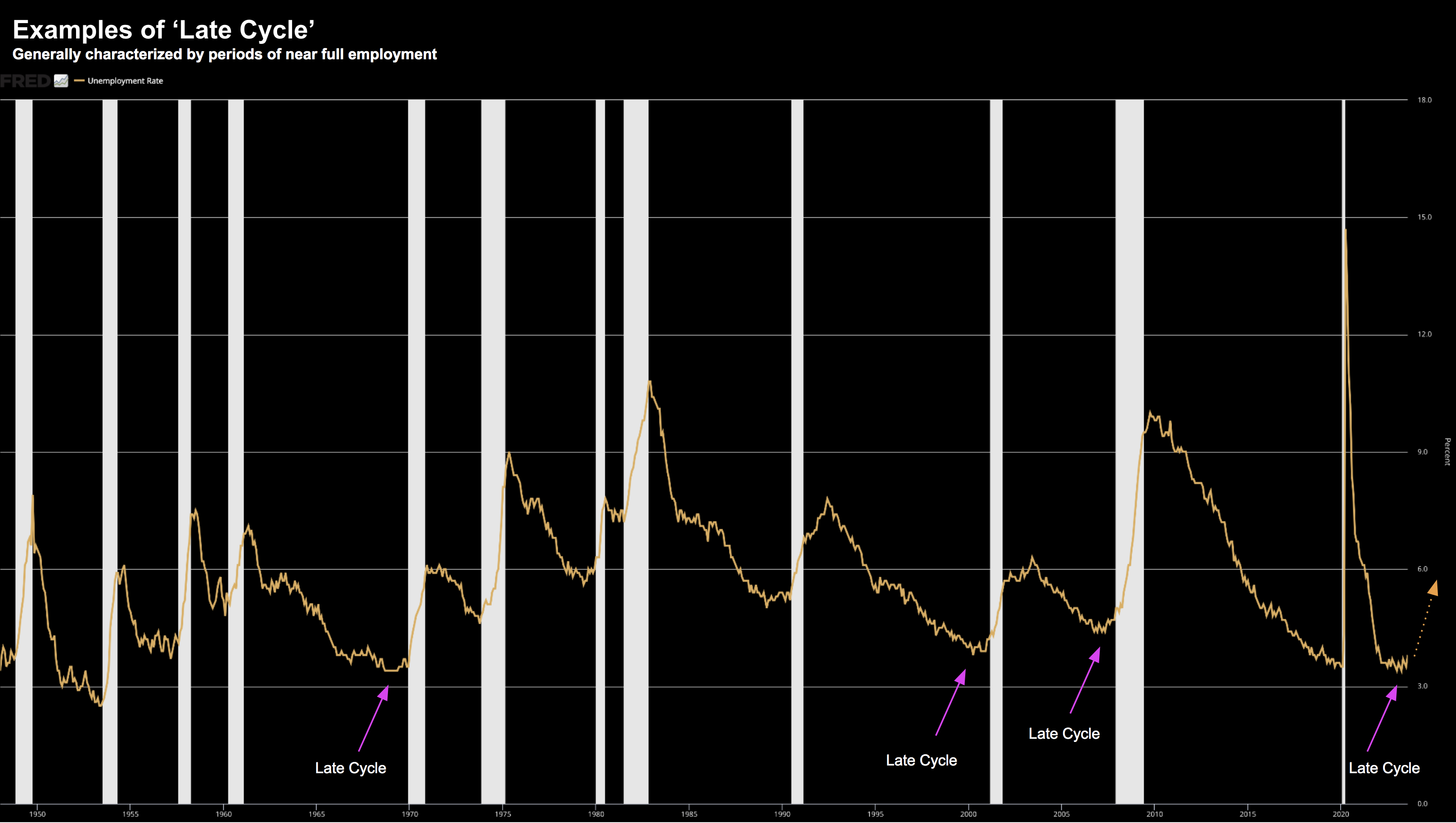

2023 has been one of the more difficult years to navigate. For example, if you chose the wrong stocks, sectors or simply decided to hide in cash - you didn't fare well. However, what's also made it hard has been the various shifts in sentiment the past ~9 months. These shifts have 'whipped' traders around. Today, with the US 10-year yield challenging almost 5.0% - the "R" word is back in the vernacular. Much of this can be explained by understanding where we are in the economic cycle... and today it's "late cycle". The challenge is navigating this phase is the most difficult of any... as it will often last longer than many expect.