AI’s Big (Depreciation) Bet

AI’s Big (Depreciation) Bet

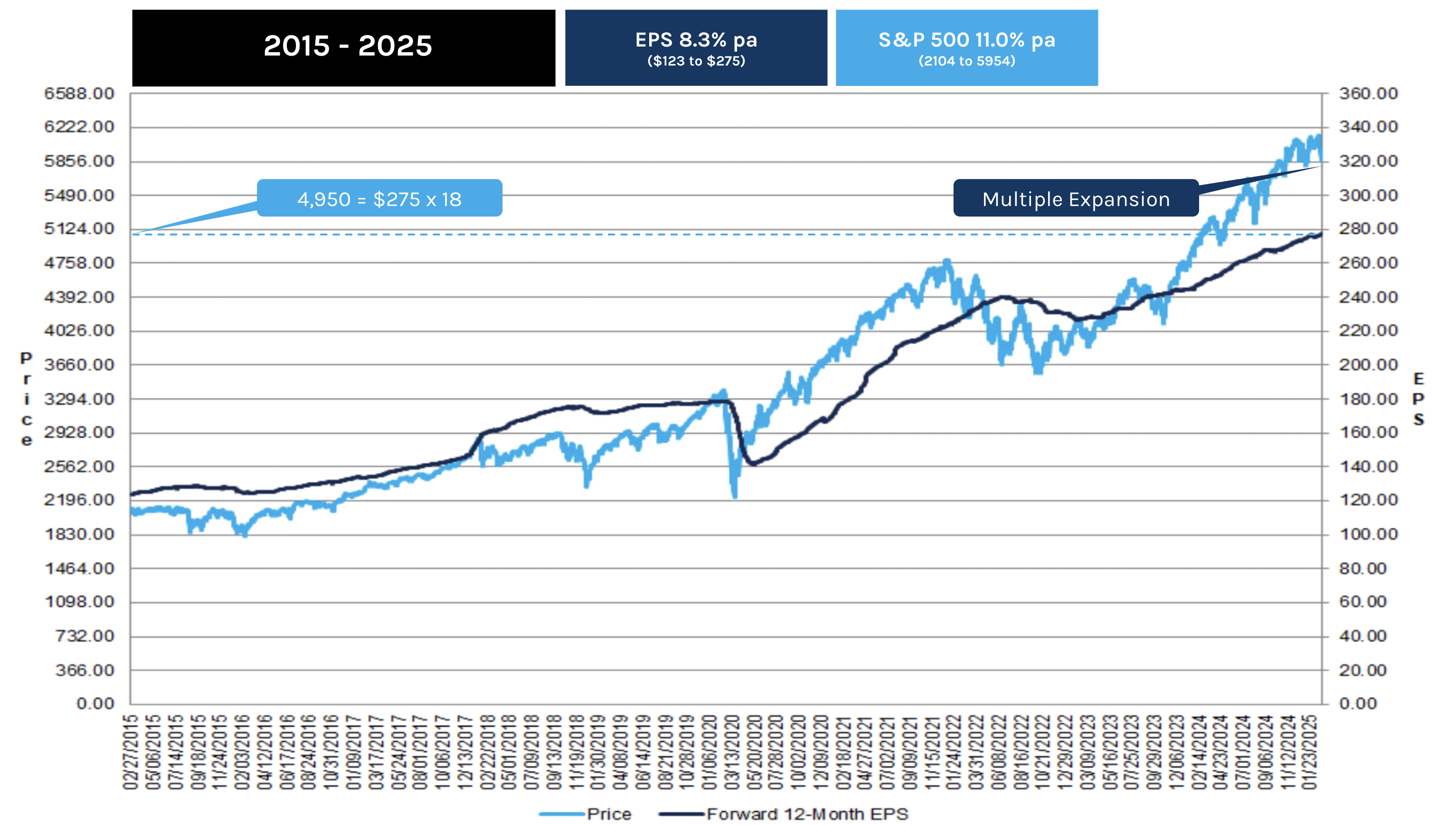

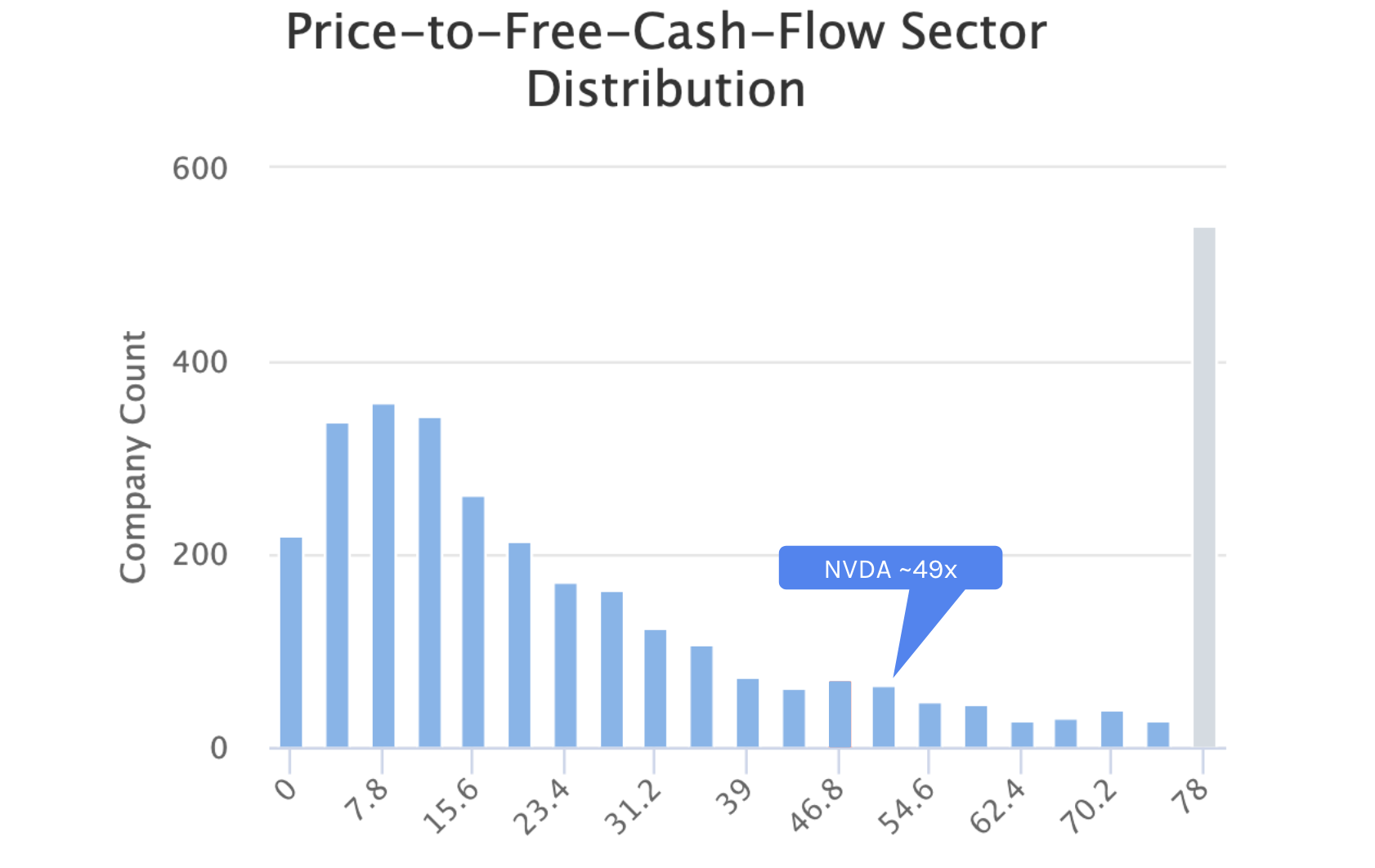

Most of the Mag 7 tech giants are using an extended 5-to-6-year depreciation schedule for their massive GPU investments. Since GPUs typically have a 3-year useful life, this practice artificially inflates current earnings by reducing the reported expense. If these chips rapidly become obsolete, investors paying high multiples must question the impact on future Free Cash Flow and margins when the true depreciation expense inevitably hits. Investors are optimistic that will show very strong returns (and soon) on their half-trillion-dollar bet.