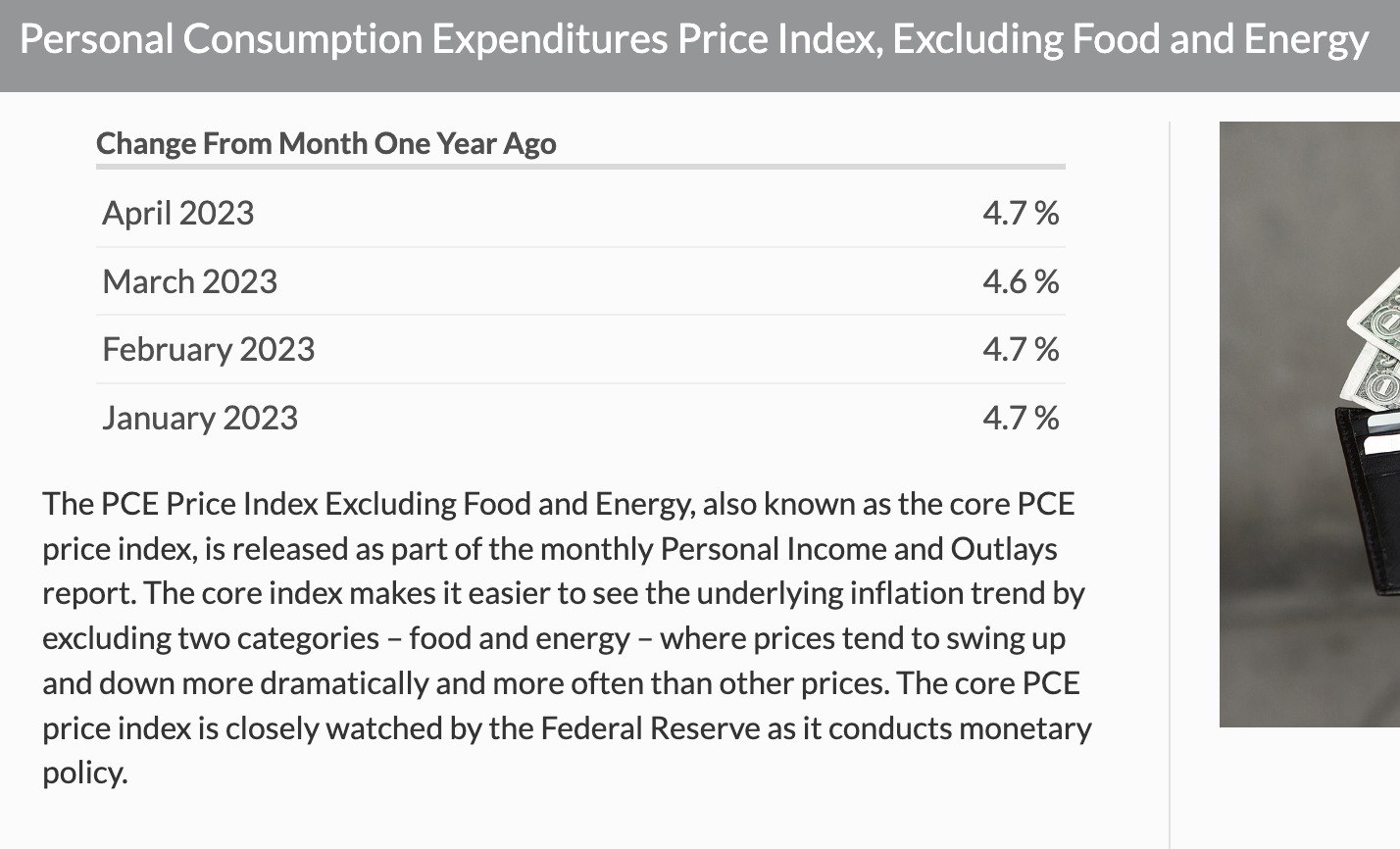

‘Higher for Longer’ after May Core PCE

‘Higher for Longer’ after May Core PCE

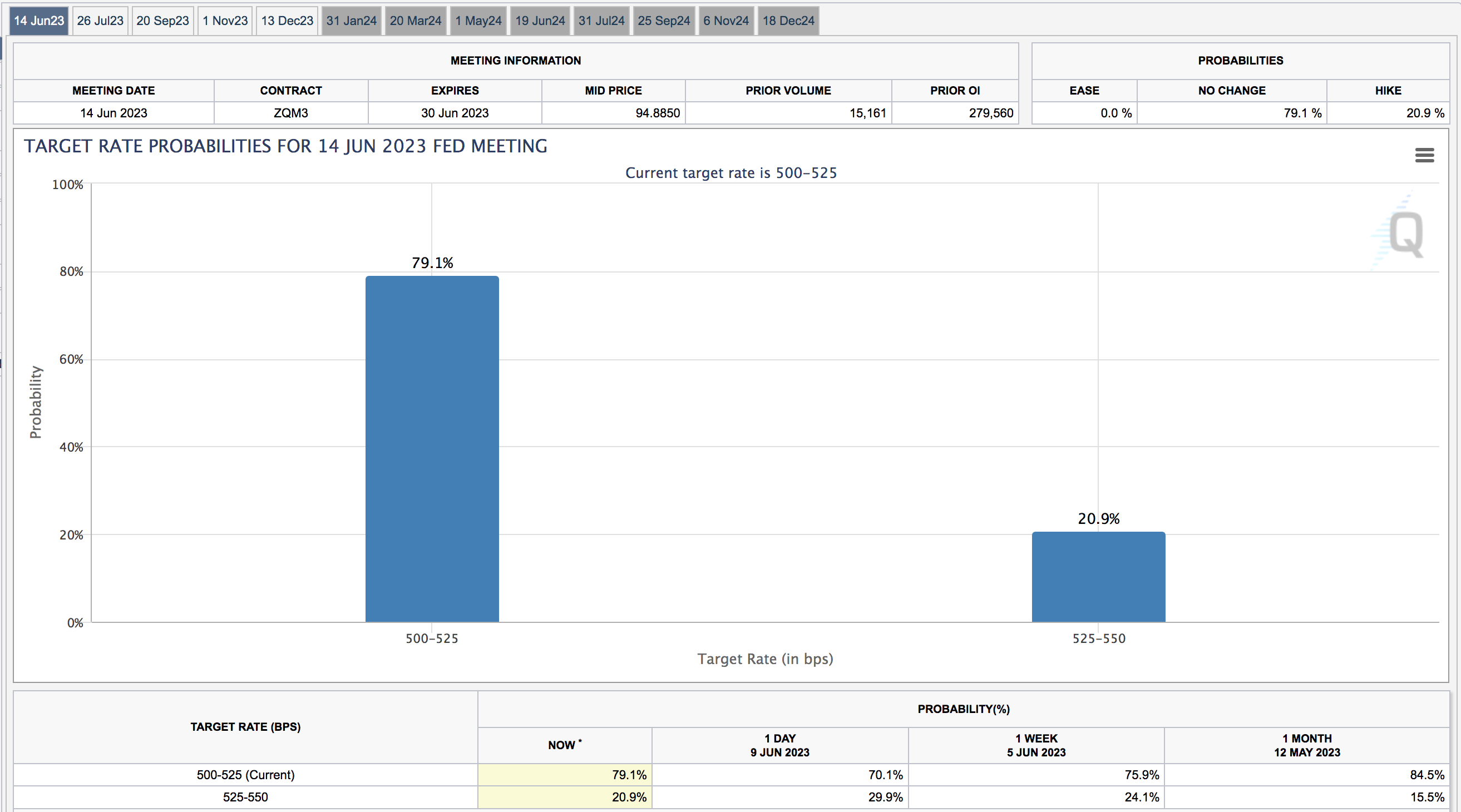

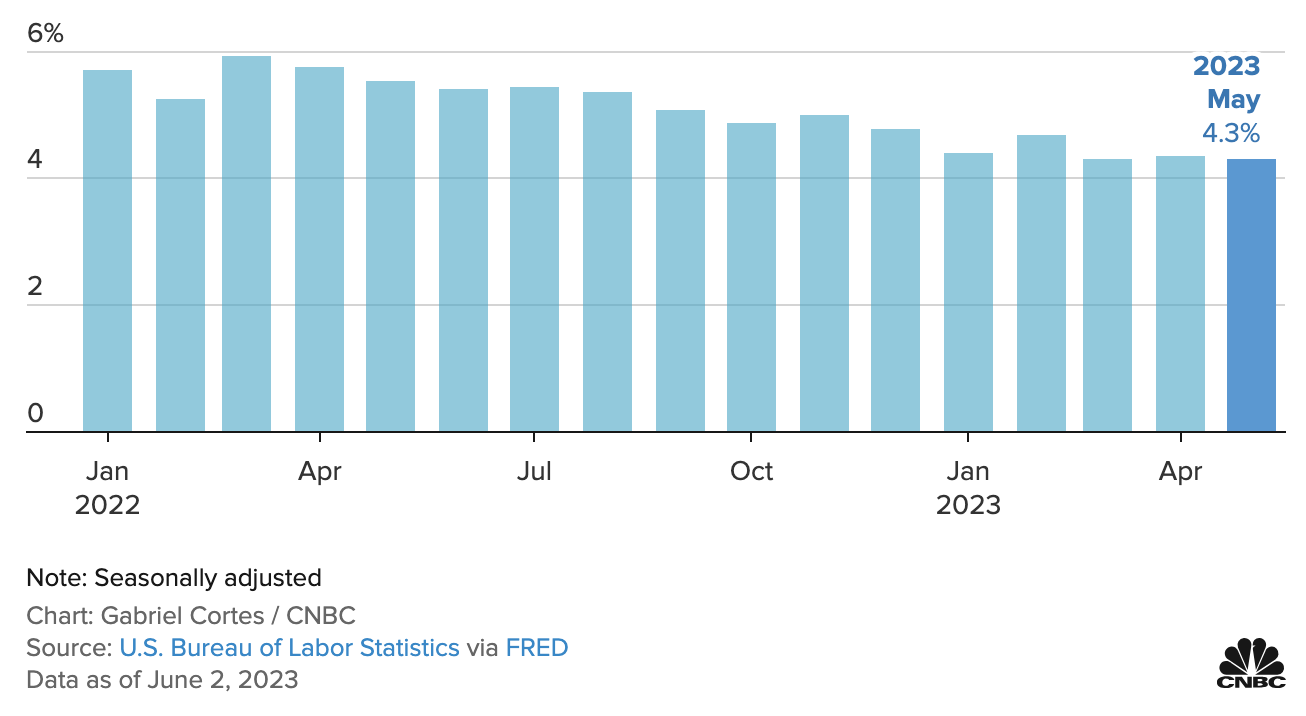

May's print for Core PCE came in 4.6% YoY - still well above the Fed's objective of 2.0%. However, mainstream were quick to label the report as 'lackluster'. Why? Here's the thing - Core PCE has hardly changed the past few months. It dipped in May to 4.62%, from April (4.68%), but was above March (4.61%), and was exactly where it had been in December (4.62%). Put another way - we have made no ground since December - and yet it was now somehow 'lackluster'. But it gets better: core services inflation (without energy services) rose by 5.4% in May YoY. It was fractionally lower than April (5.5%) - but equal to what we see in both March and December (5.4%). Similar to Core PCE - it too is stuck in a tight range for 5 consecutive months. What does all this mean? Simple: rates will be higher for longer and markets don't get it.