People Choose What They Want to Hear

People Choose What They Want to Hear

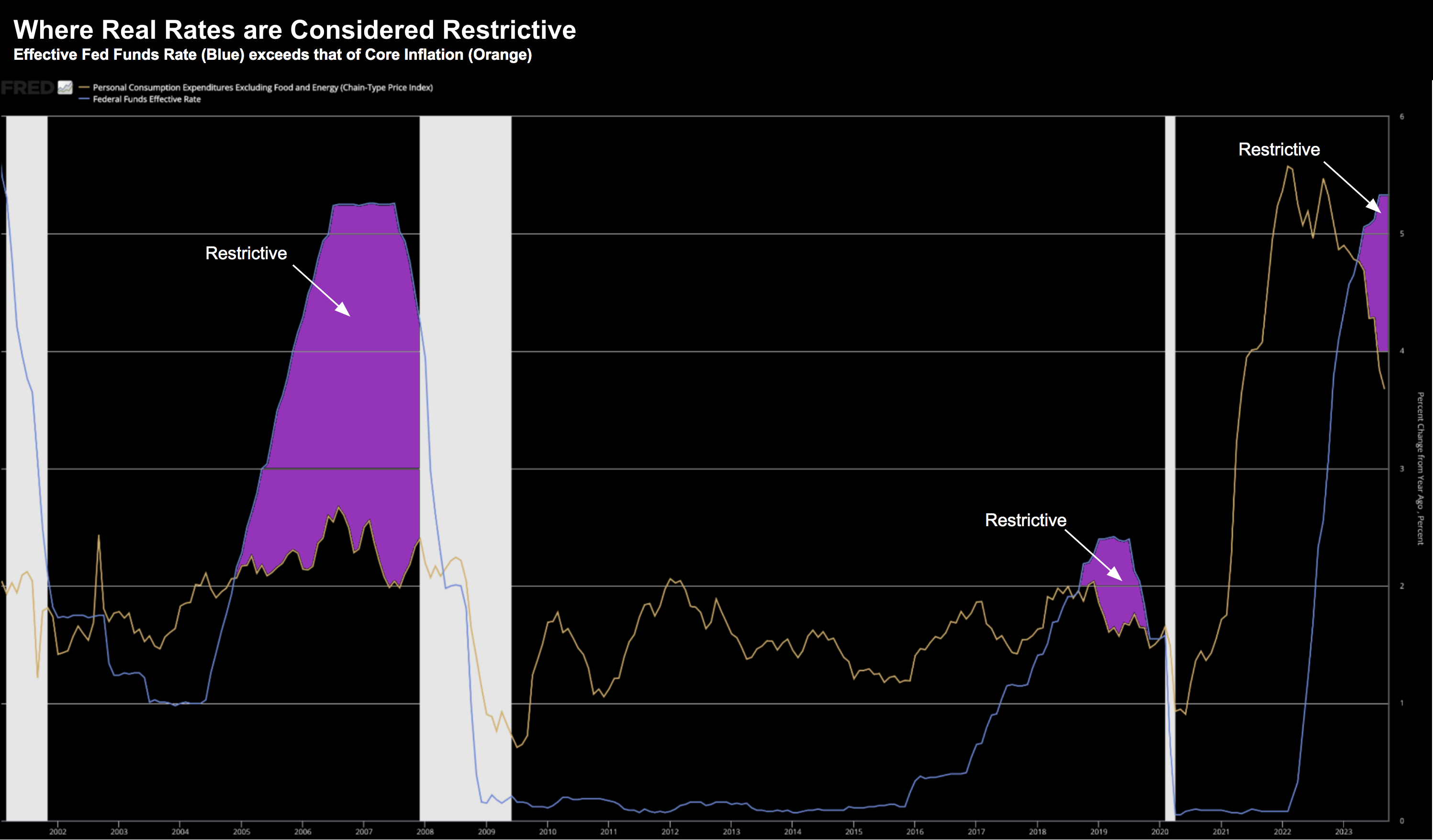

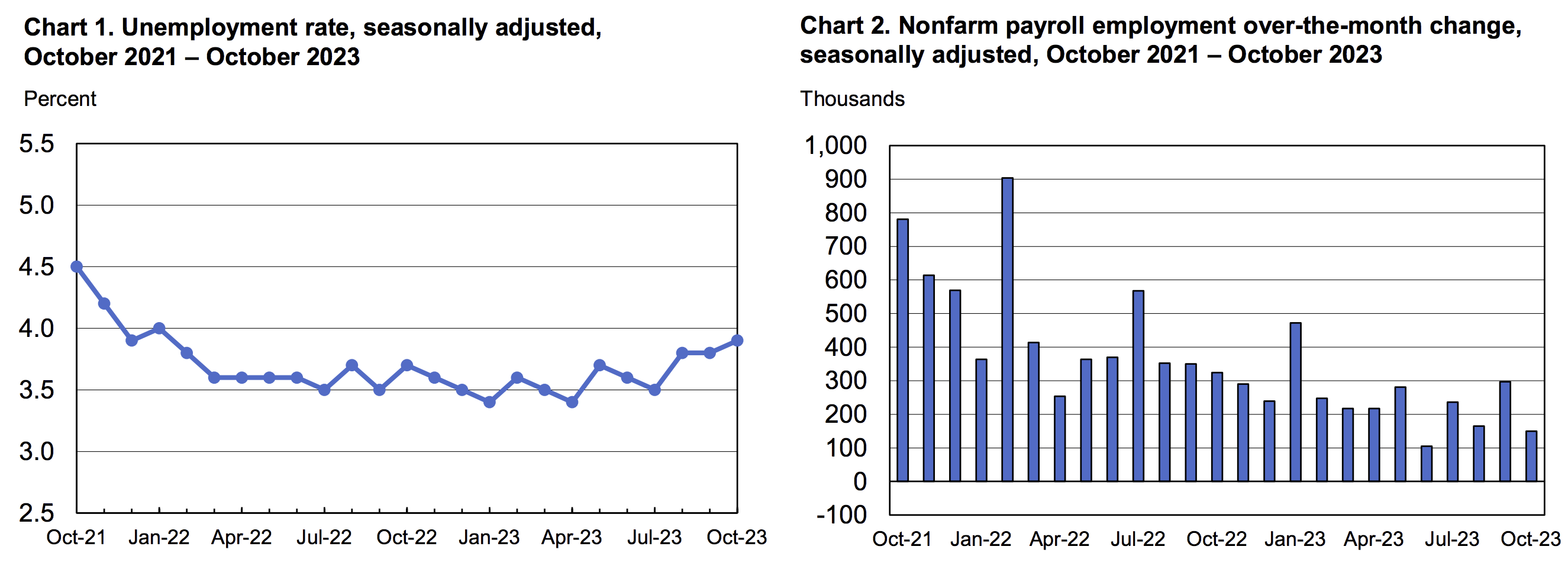

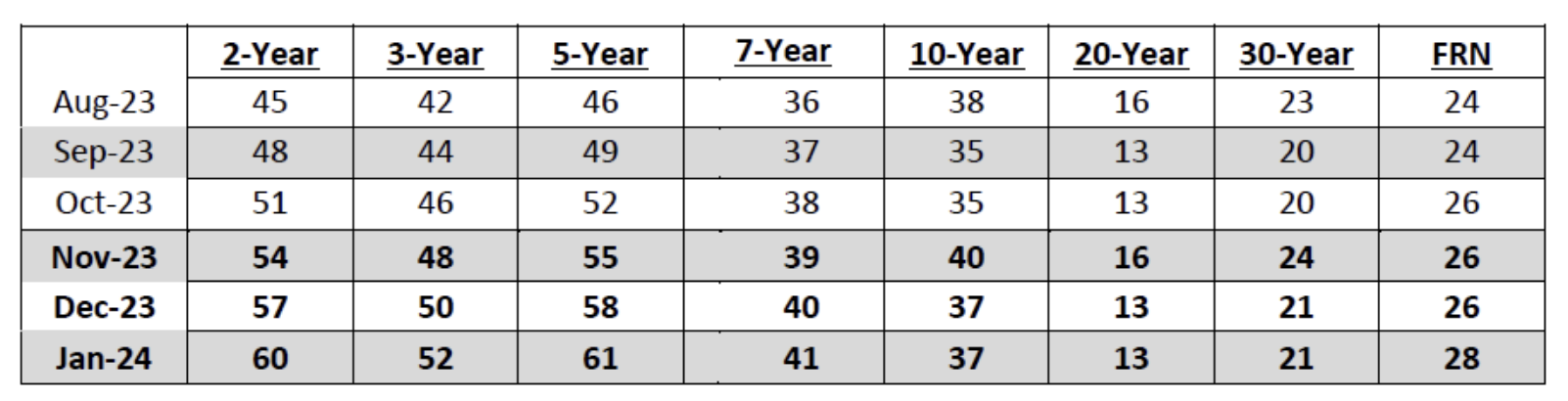

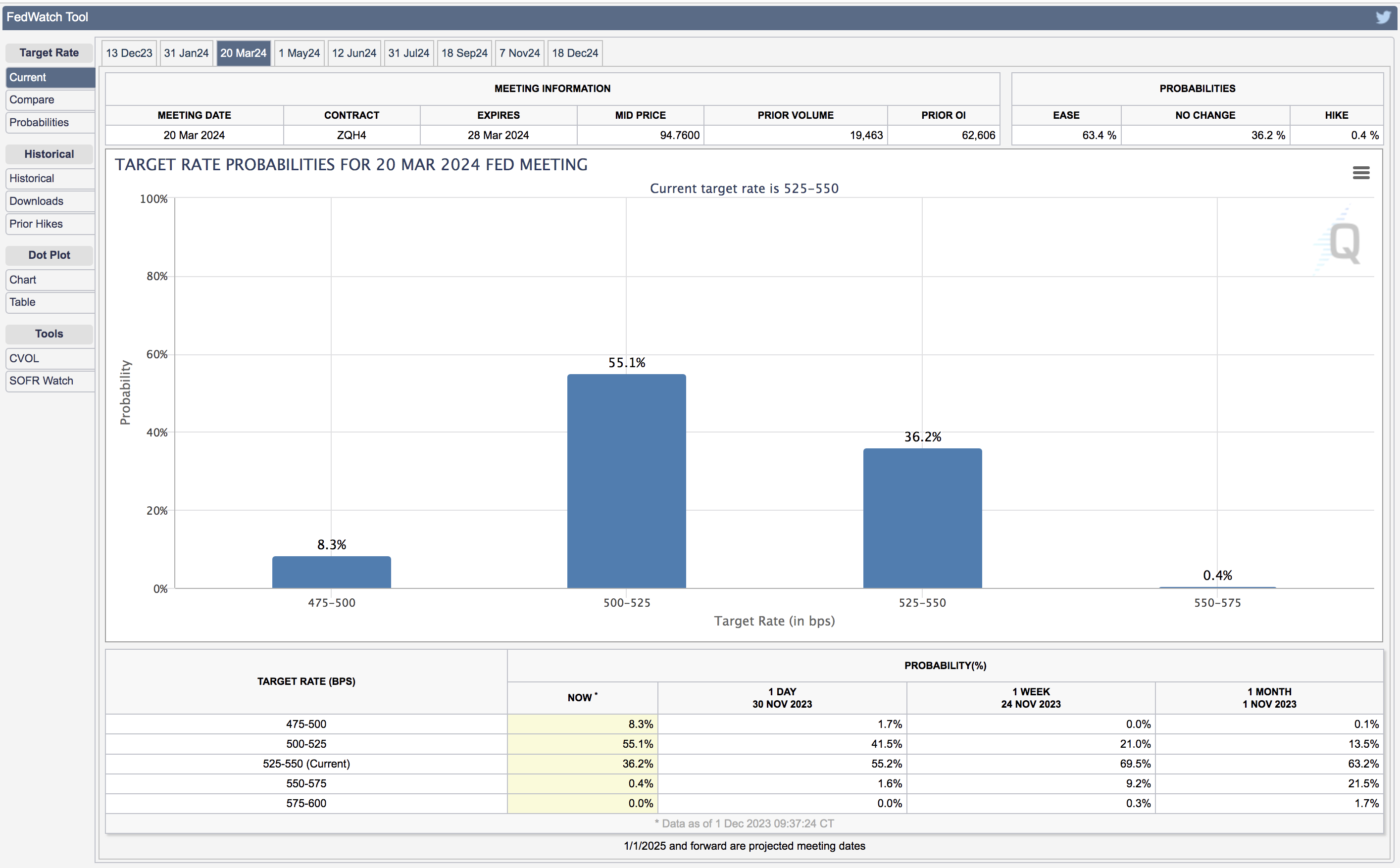

Markets continue their ascent after a blistering November. The Dow and S&P 500 each gained ~9% for the month - in what is typically a seasonally strong time of year. From a year-to-date perspective, the Dow is up 8.5%, the S&P 500 is up ~19% and the Nasdaq up over 35%. The anomaly? 493 of the 500 stocks on the S&P 500 are barely positive for the year (i.e., the equal weighted index). So what's driving the optimism? Simple: the expectation of lower yields and the Fed hitting its terminal rate. This post looks at potential blind spots for the market.